Fracking the Code - Making Sense of Your ExxonMobil Retirement Benefits

Mining through ExxonMobil’s retirement benefits program often feels like a significant project, marked by complex terminology, layered plan design, and decisions with long‑term financial implications. Periodically, you receive benefit materials and likely glance through a few sections before returning to your demanding professional responsibilities, missing the broader opportunities to promote a brighter financial future. However, a stronger understanding of your retirement benefits provides clarity and supports the thoughtful use of the resources accumulated throughout your career at Exxon.

Across every stage of service, from newer hires building momentum, to seasoned executives and engineers approaching later career milestones, a clear and practical explanation of how to optimize retirement benefits is critical. If your benefits are properly structured, you may save $5,880 - $12,025 in taxes annually, depending on your individual circumstances. Several key components within your Exxon retirement benefits structure are worthy of consideration as you align the benefits with your personal goals, financial priorities, and life beyond the workplace.

ExxonMobil Savings Plan / Voya 401(k) Plan – the 401(k) functions as the core retirement account for employees. It allows you to direct the desired amount of your pay into tax‑advantaged retirement savings. Exxon supplements your contributions through an employer retirement match. A 401(k) plan falls under a framework which generally provides strong creditor protection. Funds inside a 401(k) plan remain shielded from most lawsuits, judgments, and bankruptcy claims. Exxon provides a 401(k) because the structure supports tax‑advantaged growth, straightforward administration, and reasonable retirement asset accumulation for employees.

Key aspects of your 401(k) include:

Employee Contribution Limit – the IRS contribution limits for 2026 allow you to contribute up to $24,500. If you are age 50 or older, additional catch-up contributions are permitted. Within the Exxon 401(k) Plan, you may choose from three contribution types: pre‑tax, Roth, and after‑tax. Pre‑tax contributions reduce taxable income in the year of the contribution. Earnings on pre-tax contributions grow tax-deferred, and distributions are taxed as ordinary income when withdrawn. Roth contributions consist of after-tax dollars. The funds in the Roth subaccount within the 401(k) grow tax-free, and qualified distributions during retirement occur tax-free. Similar to Roth contributions, after-tax contributions are eligible for withdrawal in the future free of taxes, but earnings on after-tax contributions accumulate on a tax-deferred basis. Unlike Roth distributions, earnings in the after-tax subaccount prove taxable above the after-tax contribution itself, making them less advantageous relative to the Roth. Exxon’s plan permits a maximum contribution of 20% of your compensation, a unique feature of the plan.

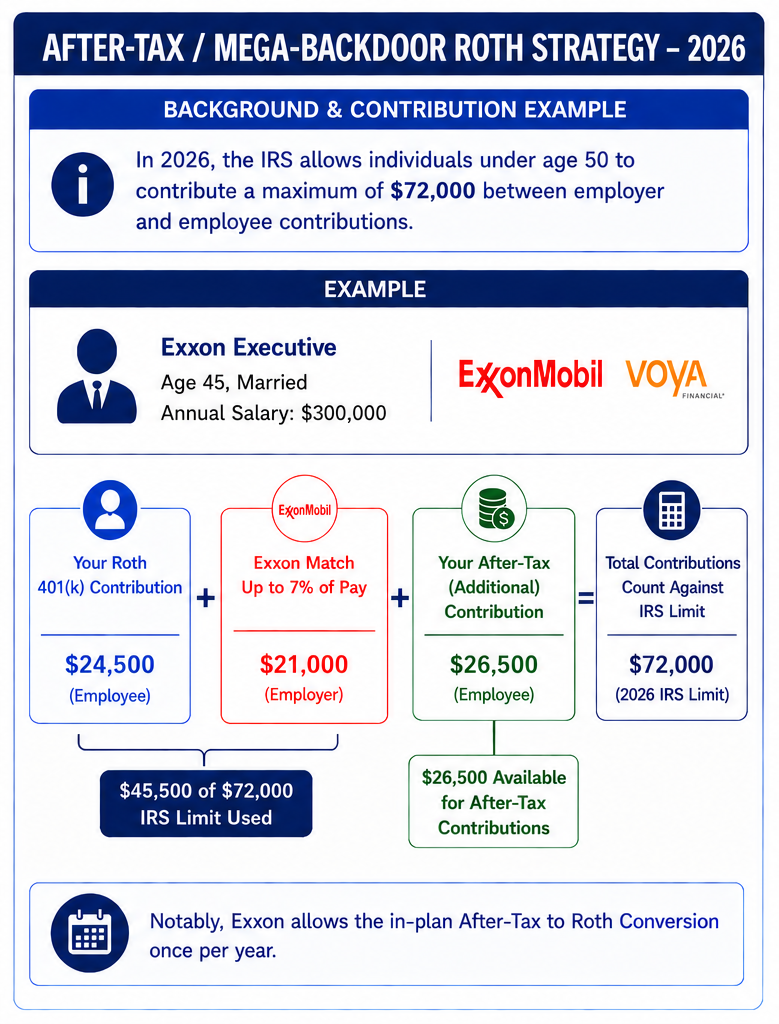

After-Tax / Mega-Backdoor Roth Strategy – in 2026, the IRS allows individuals under age 50 to contribute up to $72,000 to their 401(k) between employer and employee contributions (combined). For example, if you are an Exxon executive (age 45 and married) earning $300,000 and you are contributing the maximum $24,500 to your Exxon 401(k) at Voya, Exxon will match your contributions up to 7% of your compensation ($21,000). Between your contributions and Exxon’s contribution, $45,500 will count against the $72,000 IRS limit, leaving you with $26,500 available for additional after-tax contributions. You can potentially make after-tax contributions of up to $26,500 to the 401(k) (subject to the 20% of compensation limit) to fill up the $72,000 in allowable contributions. If the after-tax contributions are subsequently converted to Roth, this is known as the “Mega-Backdoor Roth Conversion,” a strategy which could prospectively reduce your future taxes by hundreds of thousands of dollars under the right circumstances.

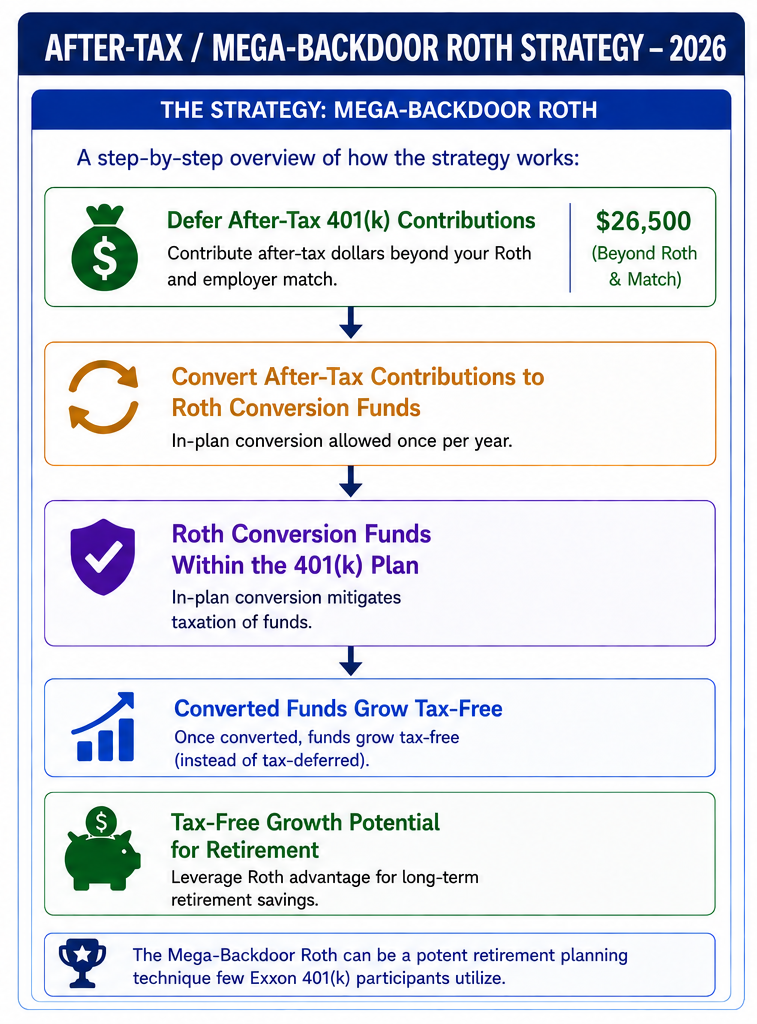

Mega-Backdoor Roth Strategy Illustration

Not all plans permit conversions to Roth inside the plan, but the Exxon 401(k) Plan offers capability to convert your after-tax contributions to Roth Conversion funds. You transfer funds from the after-tax balance to the Roth balance within the plan. To the extent there was any growth on the after-tax balance between when the contribution occurred and the conversion occurred, you pay tax (but no penalty) on the growth only. Thereafter, all growth on the after-tax balance and earnings is tax-free. Notably, Exxon allows the in-plan after-tax Roth Conversion once per year. Once again, the strategy is referred to as a Mega-Backdoor Roth and it proves a potent retirement planning technique for you. Seeking professional guidance to support the process is critical to avoid errors.

Step-By-Step Example to Complete Mega-Backdoor Conversion:

Employer Contribution Limit – as of January 1, 2026, you must contribute a minimum of 6% of your pay to receive Exxon’s 7% company match. If you contribute less than 6% of your pay, you will receive no company match from Exxon. Exxon’s match is subject to the 2026 IRS 401(a)(17) Compensation Limit for Employer Contributions, which limits the amount of income upon which Exxon matches. If you are an employee earning above the limit, Exxon utilizes other means to “make you whole” with respect to your employer contributions.

Net Unrealized Appreciation (NUA) – another benefit of working for Exxon is you can purchase XOM stock within your 401k. Purchasing Exxon stock in the 401(k) gives you the option to complete a Net Unrealized Appreciation (NUA) distribution. NUA allows for favorable tax treatment at the time an employee either resigns or retires from Exxon (other triggering events may apply). During the special election window, the IRS allows individuals to separately transfer Exxon stock into a non-retirement brokerage account to qualify for favorable tax treatment on XOM share sales, if certain conditions are met. Generally, you pay taxes on the cost basis in your shares (what you paid for the shares when they were acquired inside of the 401(k)) at ordinary income tax rates in the year of withdrawal, but the growth on the shares sold outside of the 401(k) is taxable at long-term capital gains rates, which may prove lower than your ordinary income tax rates during retirement. The NUA strategy can save you material tax dollars relative to leaving the shares in the 401(k), if your advisor and tax accountant coordinate well with you to implement the strategy. Using NUA fits best with the lowest cost basis shares you own, and there are many rules to consider. Exercising the NUA election without professional support is not advisable.

Risk Associated with Net Unrealized Appreciation (NUA) – NUA is a powerful tax savings tool available to you as an Exxon employee. One matter of which to be mindful is to avoid investing too heavily in Exxon stock through your 401(k), personal brokerage account, or Restricted Stock Units (RSUs) due to the risk of overconcentrating your net worth into only one company stock. A common mistake amongst employees of publicly traded companies is allocating a large portion of their savings to their employer’s stock, believing their more knowledgeable perspective about their company gives them an advantage in understanding the business. Unfortunately, time and time again, investors learn investing primarily in one company is often foolhardy. Enron, Lehman Brothers, Blockbuster, and CIT Bank are a few examples of companies investors believed would never fail. An astute financial advisor will help you allocate an appropriate amount of your savings into Exxon stock to keep you within the guardrails of proper allocation to company stock.

Should you contribute to the 401(k)? – the answer is likely yes! Assess if you possess a reasonable emergency fund (at least 3-6 months of expenses), and any high-interest debt is paid off first. Subsequently, consider starting comfortable contributions in the context of your personal budget.

To fully maximize your retirement benefits from your Exxon 401(k), consider speaking with a trusted advisor to learn more about the Roth vs pre-tax option, the employer contribution, and the Mega-Backdoor Roth Strategy.

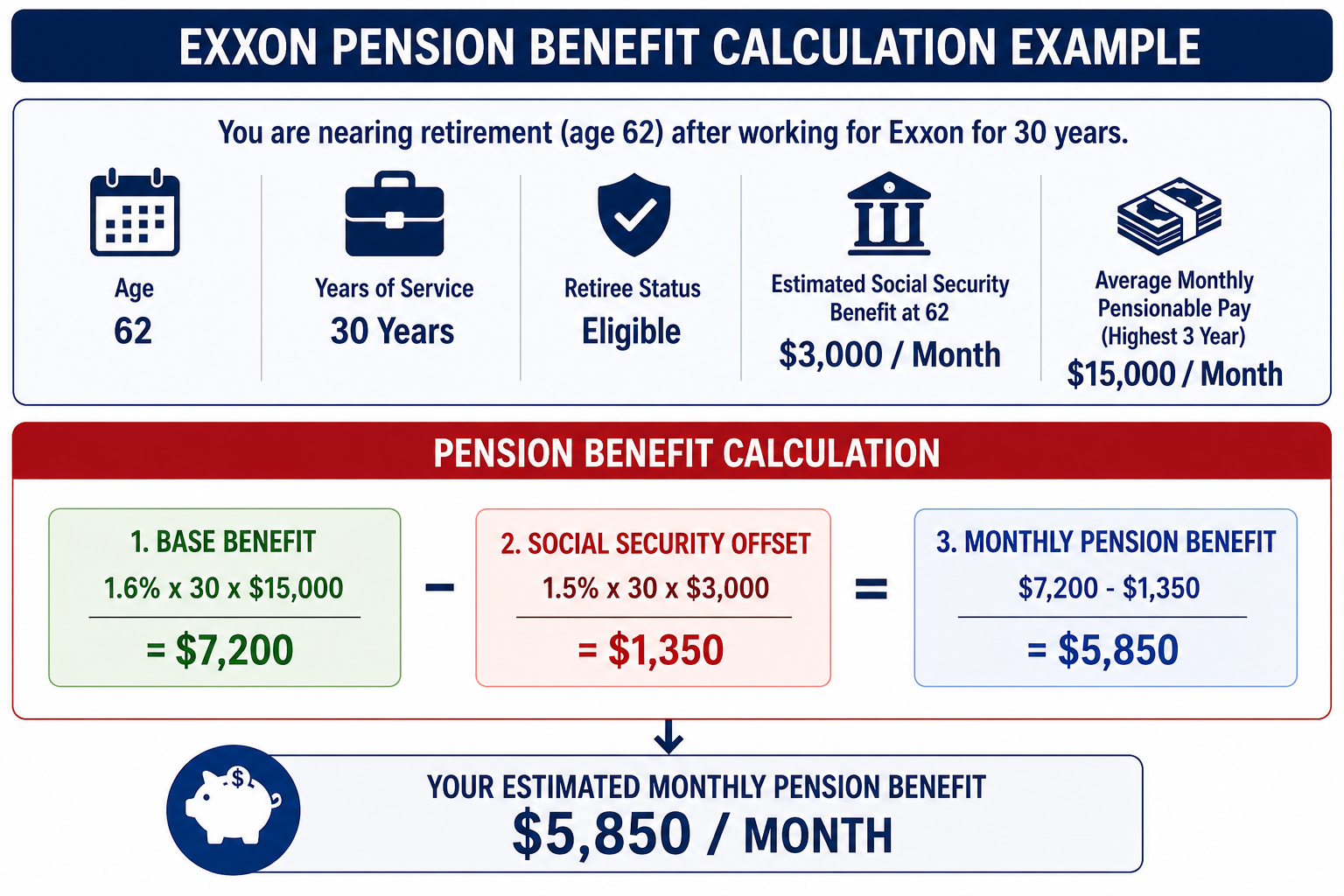

Defined Benefit Pension Plan (DBPP) – Exxon also offers a DBPP, which functions as a retirement plan under which eligible employees receive a fixed, pre-established benefit upon retirement. A DBPP is eligible for a rollover to an Individual Retirement Account (IRA) or may be claimed as a monthly annuity when an employee retires, helping to support their retirement goals. Like historical pensions more typical in the 20th century, Exxon does “guarantee” a specific monthly pension benefit from the DBPP if the annuity is claimed. To meet the minimum qualifications, an employee must work at Exxon for at least five years as a regular employee (consistently working a full-time schedule). Furthermore, if an employee meets the basic eligibility criteria, benefits are often most optimal once retiree status is attained. To reach retiree status for the DBPP, an employee needs to attain at least 55 years old and to be considered a regular employee with fifteen or more years of service. While retirement at 55 is feasible under the pension, a reduction of 5% per year occurs for every year you retire prior to age 60. Exxon calculates your pension benefit as 1.6% x years of pension service x final average pensionable pay – Social Security offset (capped at 50% maximum offset).

An example may prove edifying:

You are nearing retirement (at age 62) after working for Exxon for 30 years. Your estimated Social Security Benefit at 62 is $3,000 a month. Given your years of service and age, you meet the criteria for retiree status. Moreover, during your last three years at Exxon (note that Exxon accounts for your highest average 36 months of earnings during the last 10 years of your employment to calculate your pension), your average monthly pensionable pay equates to $15,000 a month. The calculation for your benefits is as follows: 1.6% x 30 x $15,000 – (1.5% x 30 x $3,000 Social Security Benefit) = $7,200 - $1,350 = $5,850 per month. If you elect to take the lump sum, it is based upon a balance Exxon assumes you will need to invest to generate a similar monthly benefit. See the chart below for a graphical illustration of the calculation for the monthly annuity:

Calculating your Pension Benefit

Key Details Regarding your DBPP:

Employee Contribution Limit – none are permitted.

Employer Contribution Limit – Exxon contributes the necessary portion of your income up to the 2026 IRS 401(a)(17) Limit of $360,000 to fund your future pension benefits. If you are an employee earning above the limit, Exxon utilizes other means to “make you whole” on the employer benefits. If you are a highly compensated employee, there are tax planning opportunities for Exxon’s contributions above the $360,000 income limit.

Lump Sum Distribution Option – upon retirement (or termination in some instances) an employee may elect to roll over the Defined Benefit Pension Plan (DBPP) to an Individual Retirement Account (IRA). Exxon computes the lump sum amount by examining how long you are expected to live, and current interest rates. The numbers help Exxon assess what the current value is for future monthly pension payments (stated differently, how much you would need to have invested to earn the monthly annuity amount). If an employee seeks to obtain the assumptions for their particular circumstance, visiting the ExxonMobil Benefits Service Center or calling 1-833-776-9966 is prudent.

A primary advantage of the lump sum relative to the monthly annuity is flexibility with respect to your heirs. Generally, the annuity ends when you die or within five years of your death, depending upon the option you select. With the lump sum, you are able to leave the remaining IRA balance (after the lump sum is rolled over) to your heirs.

Why the Exxon Pension Plan matters to you – a pension plan provides you with a consistent, future income stream during retirement, regardless of which distribution option you choose. Speaking with an experienced advisor will help you evaluate the most prudent distribution strategy to achieve your financial goals.

Supplemental Savings Plan (SSP) - the SSP exists because federal law restricts the amount of compensation considered for qualified plans (e.g., 401(k) plans and defined benefit pension plans). The IRS compensation cap is $360,000 in 2026 for employer contributions. Income earned above the compensation limit is not eligible for employer matching inside the Exxon 401(k). For high‑earning employees, Exxon directs excess employer match dollars into a nonqualified deferral account, often funded through a “Rabbi Trust.” If Exxon goes bankrupt, the funds in the account are not fully protected and may be utilized to satisfy company obligations. The SSP enables Exxon to fulfill the 7% employer match for employees whose pay exceeds IRS ceilings. Within the SSP, interest is credited to the employee’s account by utilizing certain benchmarks, and the employee is unable to direct how funds are invested within the account. Without such a plan, high‑earning employees would receive less than the retirement percentage promised.

Employee Contribution Limit – none are permitted.

Employer Contributions – each year, Exxon will prospectively contribute to the plan if your income is above $360,000. Income above $360,000 will receive a 7% match to the SSP like your 401(k) account. Upon retirement, the full balance accumulated in the SSP is distributed as fully taxable income to you within a short period of time following your retirement date. If you time retirement toward the end of the year, there are tax planning opportunities available. The strategy of timing retirement to reduce taxation on the SSP is specific to each individual, and seeking guidance from an experienced team is sensible.

What Exxon’s SSP contribution means for you - if you earn over $360,000 in 2026, the SSP may lead to meaningful contributions from Exxon, enabling you to accumulate more resources for your financial future.

Supplemental Pension Plan (SPP) - the SPP functions in a similar fashion to how the Supplemental Savings Plan (SSP) complements the 401(k). Instead of pairing with a 401(k), the SPP is designed to supplement the Exxon Defined Benefit Pension Plan (DBPP), primarily for high-income employees. The same IRS compensation cap of $360,000 in 2026 is applicable for eligible compensation for the DBPP, like the 401(k) plan. Employer contributions above the aforementioned compensation limit cannot fund the Exxon DBPP and instead must flow into the SPP. The SPP is not protected from creditors if Exxon experiences bankruptcy. Notably, the SPP enables Exxon to fulfill the pension benefit for employees whose pay exceeds IRS ceilings. Without such a plan, high‑earning employees would receive less than the retirement pension benefit promised.

Employee Contribution Limit – none are permitted.

Employer Contributions – Exxon calculates the lump-sum amount using the same formula as the DBPP. The calculation accounts for earnings exceeding the 2026 limit of $360,000 and assumes a monthly benefit starts at age 65, regardless of your actual age. While the standard pension permits choices between a monthly annuity payment or lump sum rollover into an IRA, the SPP plan requires a lump sum payout. Much like the SSP, Exxon distributes the entire balance as taxable, ordinary income within a short period of time following your retirement. Both supplemental plans require prudent tax planning strategies due to the large lump sum payout potential upon retirement for you.

What Exxon’s SPP benefit means for you - similar to the SSP, Exxon “makes you whole” for earnings over $360,000 in 2026. If you are one of these highly compensated employees, fruitful financial planning accounts for the lump-sum payout, considering your complete financial picture. In our experience working with highly compensated employees at Exxon, the SPP is typically more material than the SSP.

Restricted Stock Units (RSU) – an RSU program provides employees with Exxon stock as part of their compensation, subject to vesting requirements. Vesting typically relies on an employee’s continued employment over a defined period, achievement of specific performance goals, and remaining employed with Exxon versus joining a competitor. Upon vesting, the employee may choose to receive shares of stock, a full cash distribution, or a mixture of both based on the stock value upon vesting. Taxation occurs upon the stock becoming the employee’s, subject to both ordinary income and Federal Insurance Contributions Act (FICA) taxes.

Employee Contribution Limit – none are permitted.

Employer Contributions – Exxon does not grant RSUs to all employees. If you receive RSUs, the amount granted varies, but generally the vesting period follows a 7-year schedule, with 50% vesting at 3 years and 50% vesting at 7 years.

Understanding Exxon retirement benefits often feels demanding, especially as you balance your daily responsibilities at work and at home. Clear insight serves as a strategic advantage, and each plan Exxon makes available to you plays an important role in building your long-term financial security. When coordinated thoughtfully, your Exxon retirement benefits can produce meaningful tax savings for you each year, with potential savings ranging from several thousand dollars to tens of thousands of dollars based on your income level and state of residence. Elections surrounding retirement plans and pensions as you approach retirement may produce hundreds of thousands of dollars in tax savings. Professional guidance supports smarter coordination and more favorable tax outcomes for you.

Time and energy remain limited resources. Your attention outside of work likely centers on family, health, charitable interests, or personal pursuits. You likely do not desire to navigate layered benefit rules and tax considerations on your own. A capable advisory team provides you with clarity and direction, enabling confident decisions, tax-efficient investment management, proactive tax reduction strategies, proactive liability and insurance planning, clear progress toward long-range goals, and thoughtful preparation for legacy objectives.

A clear plan transforms complexity into confidence. Thoughtful use of your Exxon’s retirement benefits strengthens financial outcomes and supports a future built with intention. With knowledgeable guidance and a defined strategy, you can remain focused on what matters most while your plan works quietly in the background.

Co-Authors:

Jonathan McAlister, CFP®, CKA®

Justin Reede, CFP®, CKA®

Disclosure: The investment returns of investment securities are subject to various risks and are not guaranteed. Consult with an investment advisor representative for formal investment advice. For tax compliance advice, we recommend you consult with a CPA or Enrolled Agent. For legal advice, we recommend you consult with legal counsel. This blog post should not be considered investment or tax advice. Please note that benefit plans at Exxon are subject to change, and this article may not capture those changes. Integrity Road Wealth Partners, LLC is not affiliated with ExxonMobil Co. in any way.