Navigating Your United Airlines Retirement Plan Benefits

Navigating the United Airlines Pilots’ Benefits Program may feel like flying through a cumulonimbus cloud with no avionics given the unfamiliar terminology, programs, and choices. Many pilots receive the annual benefits guide in their inbox or review portions of the 2023 Air Line Pilots Association (ALPA) Agreement with United, scan a few lines, and return to their flying schedules without fully realizing the opportunities available. Importantly, clearly understanding your benefits may reduce your taxes while supporting long-term progress toward your financial goals. With proper optimization, first officers may save between $7,000 to $10,000 in taxes annually, and captains may reduce their annual tax burden by $10,000 to $12,000. The challenge many pilots face is sifting through each available plan and making the right elections.

From newly minted first officers, to veteran captains in the left seat, pilots benefit from a clear explanation of employee benefits. Gaining practical perspective regarding benefits available under the 2023 ALPA Agreement in plain language is critical. By approaching the details with fresh energy and curiosity, you place yourself in a stronger position to utilize your benefits to support your financial goals, priorities, and vision for life beyond the skies. The overview provided here seeks to clarify the jargon and to provide you with the insight you need to take proper action:

United Airlines Pilot Retirement Account Plan (PRAP) 401(k) - the 401(k) functions as the core retirement account for pilots. It allows pilots to direct a portion of their pay into tax‑advantaged retirement savings. United Airlines materially supplements your contributions through employer retirement contributions defined by the ALPA contract executed in 2023. Notably, employer contributions often exceed your employee contributions. United provides a 401(k) to support tax‑advantaged investment growth, selected investment options (including a self- or advisor-directed investment option), asset protection, and predictable retirement asset accumulation for pilots. Features of your 401(k) plan include:

Charles Schwab Personal Choice Retirement Account (PCRA) – the PCRA allows you to transfer funds within your 401(k) plan from the “core account” into a more flexible self- or advisor-directed brokerage account underneath the 401(k) umbrella. Your investment choices expand to a broader universe of individual stocks, Exchange Traded Funds (ETFs), and mutual funds beyond the core investment lineup. Moreover, the PCRA allows you to grant a wealth advisor access to your account to professionally manage the investments within the account on your behalf. Enabling an advisor to manage your 401(k) may unlock meaningful tax and retirement planning support not otherwise available to you as well. The right advisor will know the “ins and outs” of your benefits package at United.

Employee Contribution Limit – the IRS Contribution Limits for 2026 allow you to contribute up to $24,500 to your 401(k). You may reduce your taxes by $7,000–$12,000 each year if you max out your contributions, depending upon your tax brackets. If you are age 50 or older, additional catch-up contributions are permissible. Beginning January 1, 2026, if your FICA wages (Box 3 of Form W-2) were $150,000 or more in 2025, your aged-50+ catch-up contributions must occur on a Roth (after-tax) basis.

Employer Contribution Limit – as of January 1, 2026, United Airlines contributes a non-elective contribution (you do not need to contribute to the 401(k) to receive employer contributions) of 18% of compensation up to the 2026 IRS Compensation Limit for Employer Contributions of $360,000 in wages. If you are earning more than $360,000, United Airlines utilizes other means to “make you whole” with respect to the employer contributions.

Profit-Sharing Plan (PSP) - United Airlines maintains a profit-sharing plan (PSP) which distributes a percentage of company profits into your retirement account within the PRAP 401(k) if so elected. Alternatively, you may take the profit sharing as cash compensation. Importantly, if you defer the PSP contribution into your PRAP, you circumvent taxes during your highest earning income years. Features include:

Employer Contribution – the ALPA contract determines the exact profit-sharing percentage each year. Profit sharing is based upon different thresholds of company profitability. In 2025, profit sharing equaled 7.0585% of pilots’ compensation (paid in February of 2026).

IRS Limits – since the Profit-Sharing Plan is effectively linked to the 401(k), there are limits with respect to how much of the profit sharing is eligible for retention in your PRAP, particularly if you are consistently earning over $360,000 per year.

Winter Elections – to promote tax savings, you may elect a percentage of the profit-sharing contribution to flow into your United PRAP 401(k) each January or February.

Should you contribute to the 401(k)? – the answer is likely yes! Verify you possess a reasonable emergency fund (at least 3-6 months of expenses), and any high-interest debt is paid off first. Thereafter, consider commencing comfortable contributions in the context of your personal budget.

To fully maximize your retirement benefits from your United 401(k), consider speaking with a trusted advisor to learn more about the Roth vs pre-tax option, the employer contribution, profit sharing options, and the PCRA.

Market-Based Cash Balance Plan (MBCBP) – the MBCBP functions as a cash‑balance style pension account. Funds in the MBCBP grow tax-deferred, meaning you do not pay taxes thereon until you take distributions. A cash balance pension plan is eligible for rollover to an Individual Retirement Account (IRA) when you retire, enabling you to support your retirement goals and to continue to defer taxation. Unlike historical pensions your parents or grandparents likely received, the employer does not “guarantee” a specific monthly pension benefit from your MBCBP. The plan exists to capture employer contributions which exceed IRS limits for your PRAP 401(k). A committee is involved to determine how the MBCBP is invested. Key features of your MBCBP include:

Employee Contribution Limit – none are permitted.

Employer Contribution Limit – United Airlines does not facilitate a set contribution to the MBCBP. Instead, spillover funds from the PRAP 401(k) (the 18% non-elective contribution) are “caught” within the MBCBP since the IRS limits combined employer and employee contributions to the PRAP to $72,000 (for those under age 50).

Annual Election – an annual election must occur for the spillover funds from the PRAP 401(k) into the MBCBP and/or the Retiree Health Account (RHA).

Illustration – an enlightening, illustrative example is indicated below the RHA summary to demonstrate how the MBCBP spillover functions.

Retiree Health Account (RHA) – at United, the Retiree Health Account (RHA) helps you pay for qualified medical expenses in retirement. The RHA is formally classified as a Health Reimbursement Account (HRA) as far as the IRS is concerned. In retirement, you may withdraw funds from the RHA tax-free to pay qualified medical expenses for yourself, your spouse, and eligible dependents. Additionally, the account supports retiree health, dental, and vision insurance premium payments when the United RHA plan rules permit.

Employee Contribution Limit – under the recent ALPA contract, United deducts $1 for each working hour through mandatory salary reductions, which are excluded from gross taxable income for the pilot.

Employer Contribution Limit – there are no direct employer contributions.

Spillover from 401(k) – since the IRS limits contributions based upon earnings and specific dollar amounts for the PRAP, you are eligible to elect the PRAP “spillover” contributions from United to flow into the RHA, MBCBP, or both.

Critical Planning Consideration – if a pilot dies without a spouse and has no child under the age of 26, the RHA funds evaporate from the pilot’s estate and are reabsorbed into the United Airlines RHA Plan. In other words, all of the RHA funds are lost. Accordingly, your estate plan will impact your RHA election.

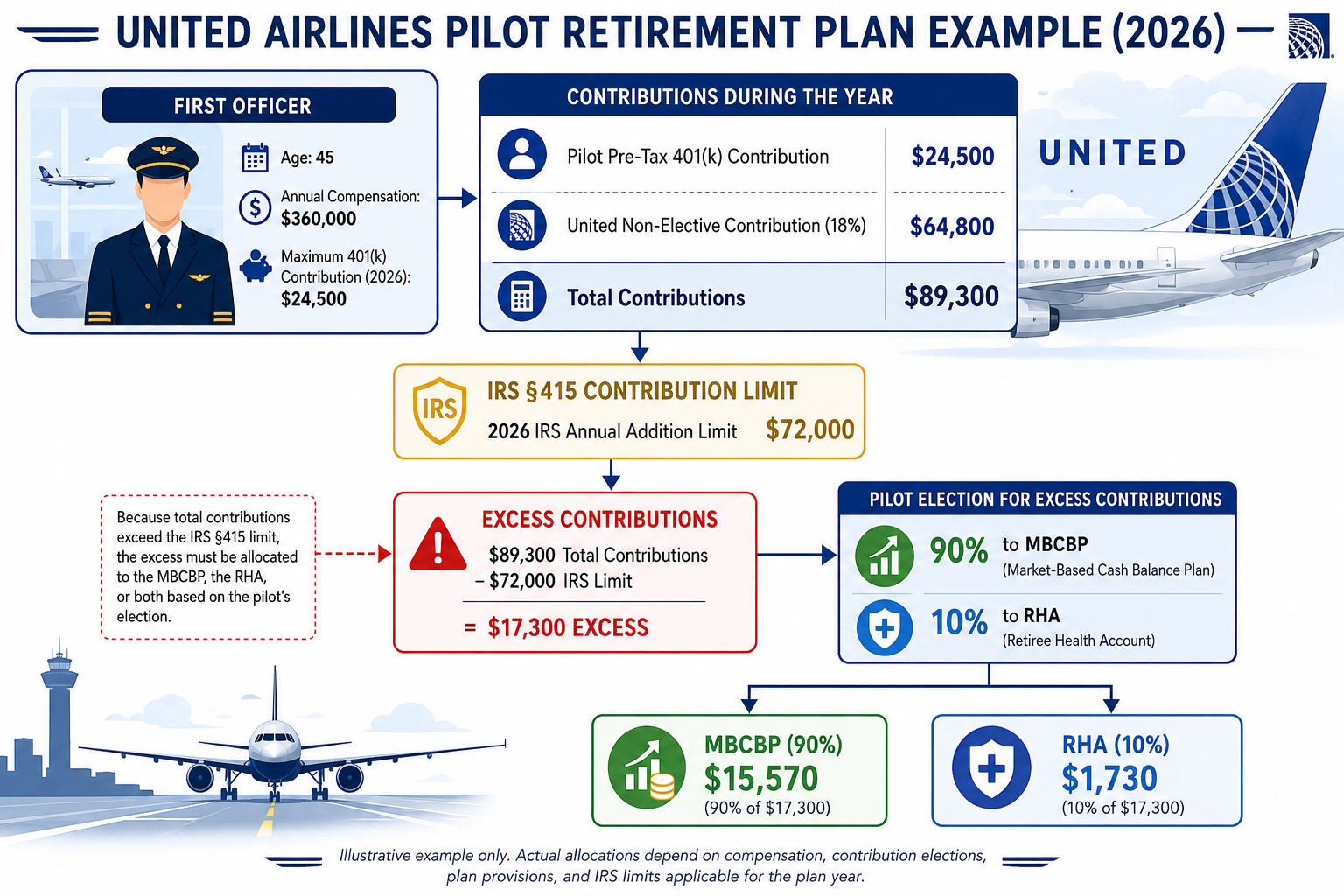

Example of PRAP 401(k) Spillover:

You are a tenured first officer earning $360,000 per year, aged 45, and contributing the maximum ($24,500 in 2026) pre-tax contribution to your 401(k). During the course of the year, you will achieve the IRS Section 415 Limit of $72,000 total allowable contributions between the employer and employee for the 401(k). Accordingly, you will contribute $24,500 to the PRAP and United would contribute $64,800 (United’s 18% non-elective contribution) but for the IRS limit of $72,000 in total contributions, for total contributions of $89,300. Since the IRS limits combined employer and employee contributions to the 401(k) to $72,000, spillover to the RHA and MBCBP could occur. You elected your overflow employer (United) non-elective 18% contributions will flow 90% to the Market-Based Cash Balance Plan (MBCBP) and 10% into your Retiree Health Account (RHA). Thus, in this example, you circumvent taxes on the $17,300 of employer spillover which will flow into the MBCBP (90% = $15,570) and RHA (10% = $1,730):

If United awards profit sharing pursuant to the Profit-Sharing Plan, additional spillover flows into your RHA and MBCBP on top of the spillover denoted in the example above. If you are unfamiliar with the mechanics of the spillover process, you are not alone. Seeking wise counsel to support you through understanding the spillover and completing the annual election between the MBCBP and RHA is critical since each pilot’s personal financial position is unique.

Understanding United Airlines’ retirement benefits often feels overwhelming, especially when flying and training already demand material time, attention, and energy. Clear information serves as a powerful asset, and each plan United offers plays a distinct role in building long-term financial security. Thoughtful coordination across the various retirement plans is likely to reduce your taxes by $7,000 to $12,000 annually, depending on where you live and your income level. Maximizing retirement planning surrounding United’s generous benefits is likely to make a meaningful difference in your financial future, so review the choices available to you carefully.

For many pilots, working with a knowledgeable advisor enables confident decision-making, tax reduction, tax-efficient investment management, estate planning awareness, risk mitigation, and steady progress toward financial goal achievement. Since time outside the cockpit often centers on family, rest, charitable interests, and other priorities, professional guidance enables you to cut through the details. Working with a fee-only wealth advisor familiar with your benefits is likely to afford you more peace of mind and time to focus on what matters most to you. Consider devoting the time to consulting with an advisor who will support you in each area of your financial life as the right next step in your financial flight plan.

Co-Authors:

Jonathan McAlister, CFP®, CKA®

Justin Reede, CFP®, CKA®

Disclosure: The investment returns of investment securities are subject to various risks and are not guaranteed. Consult with an investment advisor representative for formal investment advice. For tax compliance advice, we recommend you consult with a CPA or Enrolled Agent. For legal advice, we recommend you consult with legal counsel. This blog post should not be considered investment or tax advice. Please note that benefit plans at United are subject to change, and this article may not capture those changes. Integrity Road Wealth Partners LLC is not affiliated with United Airlines, Inc. in any way.