Confused About Your Southwest Airlines Pilot Retirement Plan? Make Sense of Your Options

Navigating the world of the Southwest Airlines Benefits Program can feel like entering a maze, filled with unfamiliar terminology, programs, and choices. Many pilots receive the yearly benefits guide in their inbox or the Southwest Airlines Pilot Association (SWAPA) Agreement with Southwest from 2020, skim a few lines, and move on with their flying schedules, never gaining a full sense of the opportunities afforded to them. A clearer understanding of the benefits available to you could materially reduce your taxes while also serving to promote your longer-term ability to achieve your financial goals. If benefits are properly optimized, first officers may save between $7,000 and $15,000 in taxes annually. Captains can prospectively reduce their annual tax burden by $20,000 - $60,000. The challenge is wading through the different plans offered to you and making the right elections.

From newly minted first officers, to veteran captains occupying the left seat, a straightforward explanation of employee benefits is desired. The overview provided in this article seeks to offer perspective regarding the benefits available under the SWAPA Agreement from 2020 in an understandable fashion, wading through the “financial speak” for you. By approaching the details with fresh energy and curiosity, you position yourself well to make choices which reflect your financial goals, priorities, and vision for life beyond the flight deck.

Southwest Airlines Pilot Retirement 401(k) Plan – the 401(k) functions as the core retirement account for pilots. It allows pilots to direct a portion of their pay into tax‑advantaged retirement savings. Southwest Airlines materially supplements your contributions through employer retirement contributions defined by the SWAPA contract executed in 2020. In fact, employer contributions for pilots often exceed your employee contributions. Southwest provides a 401(k) because the structure supports tax‑advantaged investment growth, selected investment options (including a self- or advisor-directed investment option), asset protection, and predictable retirement asset accumulation for pilots. Features of your plan include:

Charles Schwab Personal Choice Retirement Account (PCRA)– allows Southwest Airlines Pilots the option of moving funds within their 401(k) plan from the “core account” into a more flexible self- or advisor-directed account underneath the 401(k) umbrella. Your investment choices expand to a broader universe of individual stocks, Exchange Traded Funds (ETFs), and mutual funds beyond the core investment lineup. Moreover, the PCRA allows you to grant a wealth advisor / financial planner access to the account to professionally manage your investments on your behalf. Enabling an advisor to manage your 401(k) may unlock powerful tax and retirement planning support not otherwise available to you as well. The right advisor will know the “ins and outs” of your benefits package at Southwest.

Employee Contribution Limit – the IRS contribution limits for 2026 allow you to contribute up to $24,500 to your 401(k). You may reduce your taxes by $5,000 - $10,000 each year if you max out your contributions, depending upon your tax brackets. If you are aged fifty or older, additional catch-up contributions are permissible, further reducing your taxes.

Employer Contribution Limit – as of January 1, 2026, Southwest Airlines contributes a non-elective contribution (the pilot does not need to contribute to the 401(k) to receive employer contributions) of 18% of compensation up to the 2026 IRS Compensation Limit for Employer Contributions of $360,000 in wages. If you are a pilot earning more than $360,000, Southwest Airlines utilizes other means to “make you whole” with respect to the employer contributions.

Should you contribute to the 401(k)? – the answer is likely “yes!” Make sure you have a reasonable emergency fund in place (at least 3-6 months of expenses), and any high-interest debt is paid off first. Thereafter, consider starting comfortable contributions in the context of your personal budget.

To fully maximize your retirement benefits from your Southwest 401(k), consider speaking with a trusted advisor to learn more about the Roth vs pre-tax option, the employer contribution, and the PCRA.

Market Based Cash Balance Plan (MBCBP) – the MBCBP functions as a cash‑balance style pension account. A cash balance pension plan is eligible for rollover to an Individual Retirement Account (IRA) when you retire to help support your retirement goals. Unlike historical pensions your parents or grandparents may have received, the employer does not “guarantee” a specific monthly pension benefit from your MBCBP. Southwest Airlines contributes a fixed percentage of your pay (2%) into the plan, and the value grows according to the performance of underlying investments. The MBCBP exists in part to capture employer contributions which exceed IRS limits for the 401(k) available to pilots. Here are some of the key details regarding your MBCBP:

Employee Contribution Limit – none are permitted.

Employer Contribution Limit – as of January 1, 2026, Southwest Airlines contributes 2% of your income up to the 2026 IRS 401(a)(17) Limit of $360,000. If you are a pilot earning above the limit, Southwest Airlines utilizes other means to “make you whole” on the employer contributions. If you are a captain or high-earning first officer, there are tax-efficient ideas for Southwest’s contributions above the $360,000 income limit.

Spillover from 401(k) – since combined employer and employee contributions to your 401(k) are limited to specific dollar amounts, some employer contributions from your 401(k) may “spill” (fund) into the MBCBP to protect them from taxation.

Profit Sharing Plan (PSP) - Southwest Airlines maintains a long‑standing profit sharing plan (PSP) which distributes a percentage of company profits into pilot retirement accounts at Empower. The program functions as an employer contribution arrangement, similar to the employer contributions received in your 401(k) and MBCBP. Southwest Airlines indicates the purpose of the profit‑sharing system is to “reinforce a collaborative culture, reward strong company performance, and build retirement wealth across the pilot group.” Importantly, the plan helps you circumvent taxes during your highest earning income years. Features include:

Employee Contributions – none are permitted.

Employer Contribution Limit – as of January 1, 2026, Southwest Airlines contributes to pilots’ accounts: 3.5% of income, 7% of income, or the amount determined per calculations based upon actual profit (most recently, 1.1%). If you are a pilot earning above $360,000, Southwest Airlines utilizes other means to “make you whole.”

Rollover Option – if you are age 59.5 or older, Southwest Airlines allows you a once per calendar year tax-free rollover into your 401(k) Plan (which has more flexible investment choices). If you are under the age of 59.5 with five or more years of service, a one-time transfer of some or all of your balance is eligible for rollover into your Southwest 401(k) Plan. Seriously considering the rollover option is prudent since the 401(k) offers materially more flexibility.

Fall Elections - notably, every fall, you need to elect the percentage of the profit sharing contribution to allocate to your Southwest Profit Sharing Plan, 401(a)(17) plan (defined below), 415 plan (also defined below), or for payment as wages / cash. Your elections are what may reduce your taxes materially.

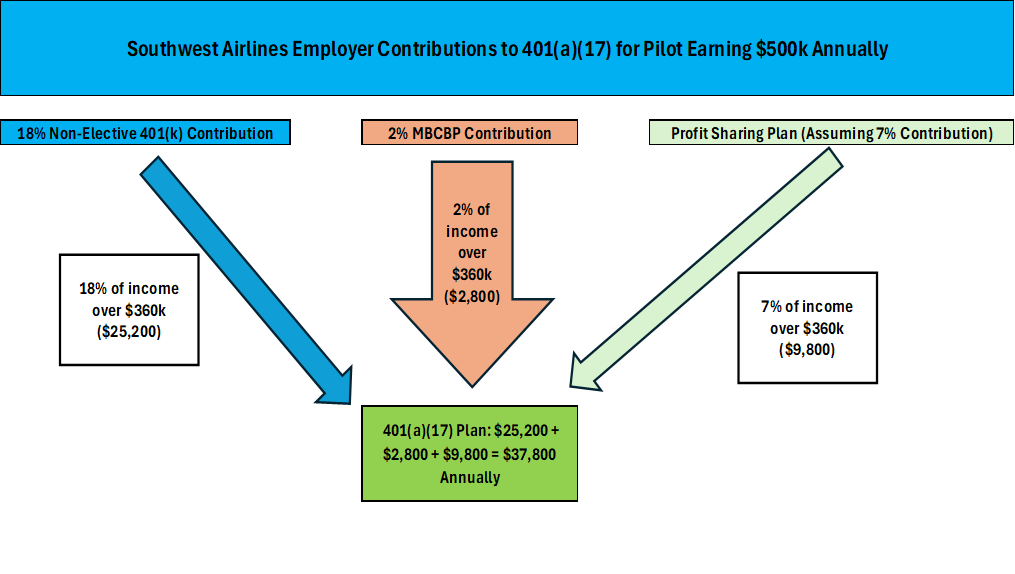

401(a)(17) Plan - the 401(a)(17) Plan exists because the IRS restricts the amount of your pay which is eligible for employer contributions to traditional tax-advantaged plans like your 401(k), Southwest Profit Sharing Plan, and pension. You may hear the term “deferred compensation (comp) plan” or “Rabbi Trust” used interchangeably with the term “401(a)(17) plan” (as if all of the financial-speak acronyms were not confusing enough). Broadly, the 401(a)(17) Plan offers you the ability to defer taxes until retirement on employer retirement contributions if your income is more than $360,000 (the IRS’ 401(a)(17) limit). More pointedly, as a pilot, you are typically paying taxes at the 32% or 35% federal tax rate (not to mention state income taxes if you live in Maryland, California, Illinois, Georgia, Colorado, Arizona, or another state with state income taxes in which Southwest has a “focus city”). If you are likely to be in a lower tax bracket in retirement, your 401(a)(17) plan is potentially a powerful tax reduction tool.

Notably, the 401(a)(17) plan is not creditor protected in the event of company bankruptcy. As a result, many pilots choose to take the excess employer contributions as cash instead of deferring them to the 401(a)(17) plan, remembering airlines like Spirit which experienced bankruptcy multiple times. In certain instances, taking excess employer contributions above $360,000 as cash makes good sense, but the right choice will differ from pilot to pilot based upon your personal financial plan, age, and tax bracket. Key features of the 401(a)(17) plan include:

Employee Contribution Limit – none are permitted.

Employer Contributions – each year, Southwest may make contributions based upon your compensation at 18% for your 401(k), at 3.5% or 7% for your profit-sharing plan (or less if profit is lower), and at 2% for your MBCBP. For the employer contribution based upon income above $360,000, you are able to decide what happens. For example, if you are captain earning $500,000 per year, you can choose to defer the following amounts into the 401(a)(17) plan, or to receive them as taxable income / cash:

Should you ask Southwest to contribute to the 401(a)(17) plan for you? It depends upon where you are in your retirement planning journey. If you are seeking a resource to support you with the deferral decisions and analysis for your 401(a)(17) plan, we are glad to serve as a resource. Generally, higher earning pilots closer to age 65 are better served by the 401(a)(17) Plan. Some pilots may save $10,000 - $15,000 in taxes by participating in the 401(a)(17) Plan each year.

415 Excess Benefit Plan – Southwest offers you a second deferred compensation plan as well. Similar to how the 401(a)(17) plan functions for employer contributions based upon your income above $360,000, there is a second limitation from the IRS on how much you can contribute to retirement plans like your 401(k): you are limited to $72,000 in total contributions in 2026 (combined employer and employee) if you are under the age of 50. Particularly if you are diligent in saving for the future, you may already be maxing out your 401(k), and Southwest is already contributing another $47,500 on top of your contributions. This does not leave any room for tax-deferred profit-sharing contributions to the Southwest Profit Sharing Plan on your first $360,000 of income.

Enter the “Excess Benefit Plan,” which can receive the overflow profit sharing plan amounts for income under $360,000: suppose you are a pilot earning $500,000 per year. You have already maxed out your 401(k), and Southwest’s contributions to your 401(k) already push you over the $72,000 annual contribution limitation (combined) for your 401(k) and profit sharing plan. If Southwest elects to award 7% of your salary from profits (i.e., $35,000), the profit sharing could not flow into the tax-advantaged Southwest Profit Sharing Plan, because you already attained the IRS contribution limit. In this example, you could choose the following for the employer contribution (no employee contributions from your wages are permitted for the 415 plan):

7% profit sharing allocation times $360,000 = $25,200 deposited into your 415 Excess Benefit Plan (so you do not pay taxes on the contribution until after retirement).

7% profit sharing allocation times $140,000 (amount above the other IRS limit of $360,000 in income) = $9,800 deposited to the aforementioned 401(a)(17) Plan.

Should you ask Southwest to contribute to the 415 plan for you? Like the 401(a)(17) plan, the 415 plan is not creditor protected. Thus, while there is a tax advantage since you circumvent taxes on the $25,200 (in the example above) in contributions until you are in a lower tax bracket after retirement, you may choose to take the payment as cash if you are concerned about creditor protection. Consult with a trusted wealth advisor / financial planner regarding the best path.

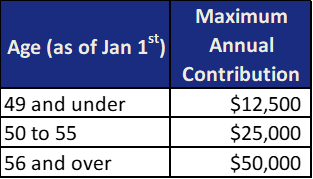

Top Hat Plan – depending upon your income, you may have access to one final tax-deferred account offered by Southwest to help you reduce your taxes. The Top Hat Plan is a voluntary deferred compensation program for pilots meeting certain income thresholds (to qualify in 2026, a pilot’s 2024 compensation must have exceeded $250,000). Pilots may contribute income to the Top Hat Plan to save on taxes today, with funds distributed after retirement when you may be in a lower tax bracket. As a nonqualified plan, assets associated with the Top Hat Plan remain subject to the airline’s creditors if bankruptcy occurs. However, contributions could save you as much as $23,000 in taxes if you are a senior captain in a state with income taxes. There are employee contribution limits:

Employee Contribution Limit – see the chart below.

Employer Contribution Limit - when a pilot contributes to the Top Hat Plan, the contribution is not considered when determining Southwest’s regular employer profit sharing plan (typically 3.5% or 7%) or 401(k) contributions (18%). To “make the pilot whole,” Southwest contributes additional money into the Top Hat Plan to reconcile the difference.

Employee Stock Purchase Plan (ESPP) – Southwest also offers you an Employee Stock Purchase Plan, which enables you to buy LUV stock at a discount. We address this topic in our article “Southwest Airlines ESPP: What Pilots Need to Know,” as the limitations are more complicated to explain. Notably, it is generally best to maximize other retirement planning vehicles (401(k), IRAs, deferred comp plans), prior to contributing to an ESPP. Contributions to an ESPP often make the most sense for the most frugal pilots who have first “maxed out” all other “tax advantaged buckets” described above.

Understanding the structure of Southwest Airlines retirement benefits may feel like a chore, especially when flying (not to mention training) already requires much attention and energy. Clear information becomes a powerful asset, and each plan outlined above plays a distinct role in shaping long‑term financial security. Notably, appropriate coordination of the various plans could save you between $7,000 - $50,000 in taxes annually, depending upon where you live and your income. Accordingly, it is worth effort to seek out an advisor to guide you to maximize your tax savings. Furthermore, since your focus outside of work likely rests with your family, rest, charitable pursuits, or other priorities, you may not wish to wade through all of the complexity alone.

Guidance from a knowledgeable team creates space for confident decisions, tax reduction, tax-efficient investment management, a reduction of risk with respect to estate planning, careful planning around liability insurance, and steady progress toward your financial goals. Maximizing your retirement planning given Southwest’s generous benefits is likely to help you make a meaningful impact on your financial future, so consider the options available to you carefully.

Co-Authors:

Jonathan McAlister, CFP®, CKA®

Justin Reede, CFP®, CKA®

Disclosure: The investment returns of investment securities are subject to various risks and are not guaranteed. Consult with an investment advisor representative for formal investment advice. For tax compliance advice, we recommend you consult with a CPA or Enrolled Agent. For legal advice, we recommend you consult with legal counsel. This blog post should not be considered investment or tax advice. Please note that benefit plans at Southwest are subject to change, and this article may not capture those changes. Integrity Road Wealth Partners, LLC is not affiliated with Southwest Airlines Co. in any way.