I Recently Lost My Job as a Spirit Airlines Pilot. What Should I Do Now?

With the recent news of Spirit Airlines officially ceasing operations as of Saturday, May 2, 2026, many Spirit pilots are left wondering what to do next. You may be one of these pilots: like most other Spirit employees, you found the announcement more abrupt than expected. Unfortunately, with rising fuel prices, challenged company leadership, and the failed JetBlue acquisition in 2023, the end of the airline came to pass.

Many pilots like you are wondering how the loss of your job with Spirit will impact your finances. What practical next steps should you take to navigate employer benefits? What should you seek in a new role? As you seek to meet your financial goals in the wake of these circumstances, there are several actions you can take with respect to your budget, healthcare plan, retirement plan, and the search for a new role to afford a hopeful financial future:

Spirit Airlines Pilot Financial Checklist:

Review Your Spending – analyzing your current spending is valuable to avoid longer-term, challenged financial outcomes. Depending upon your timeline for finding new employment, you may wish to consider making a few adjustments in simpler budgeting areas:

Reduce Dining Out - consider preparing more meals at home to manage costs and improve your overall well-being.

Subscriptions (Netflix, Hulu, Spotify, etc.) -often you will find subscriptions you are not utilizing or underutilizing which you can cancel.

Your Home and Car(s) – perform only essential maintenance on your car and home (if applicable). Defer on the “big ticket” items until you locate a new position.

Modify Housing - consider seeking alternative living accommodations. Housing often consumes the largest portion of your budget, and finding more cost-effective options will allow you to free up critical cash flow between your jobs.

Health Insurance – as of May 2, 2026, all health insurance benefits ended, including your medical, dental, and vision coverages. Given the termination of your coverage, you may apply for benefits under the Consolidated Omnibus Budget Reconciliation Act (COBRA) with 102% of the total premiums requiring payment by you directly. Spirit Airlines does not subsidize any of the costs as the airline did while you were working. Unfortunately, your COBRA coverage will end on May 31, 2026, and you will need to find other coverage options beginning June 1, 2026. Notably, there are a few options:

Private Health Insurance (this is often the best option, but many people are not aware of it!)

Your Spirit Airlines Schwab 401(k) – the Spirit 401(k) Plan through Charles Schwab also terminated as of May 2, 2026, and you will need to elect one of the options denoted below by Friday, July 21, 2026. Additionally, any 401(k) loan balances need to settle (i.e., you will likely need to determine how best to pay the balance off) as well.

Options Available for your 401(k) Include:

Rollover to New Employer Sponsored Plan – if you find a new job within the election window, your new employer’s retirement plan may allow you to roll over your Spirit 401(k) funds into your new 401(k) plan. Each 401(k) plan is different, and you will want to speak to your benefits department to determine eligibility. Notably, 401(k) plans generally contain more limited investment options than an Individual Retirement Account (IRA) and many not allow for professional management by an advisor if you would appreciate support.

Rollover to IRA – an IRA can receive your Spirit 401(k) funds and allow for materially more investment optionality. Moreover, an IRA allows for an experienced financial planner to professionally manage the account in alignment with your financial goals. Hiring a financial planner would unlock support for you in each of the planning areas defined in this article as well.

Distribute Funds Directly to You – this is often the least desirable option because you may owe ordinary income taxes (regardless of age) plus a 10% distribution penalty if you are age 59 ½ or younger. If you withdrew the balance as a lump sum already, you do have 60 days to roll the balance into an IRA with limited tax impact.

Each pilot’s situation is unique, and in some cases a combination of the three options may prove appropriate. An experienced financial planner will help you determine which approach best aligns with your needs and financial goals.

Unemployment Benefits – as you are actively seeking future aviation employment, utilizing unemployment benefits in the interim is prudent. Many people do not realize the unemployment benefits received (if eligible) are considered taxable income, so it is critical to plan accordingly. Speak with a tax professional to determine if your tax withholding is prudent.

Action to Take - click here to find step by step instructions regarding how to apply for unemployment benefits from the U.S. Department of Labor. Importantly, each state manages the administration of benefits.

Obtain Tax Documents – at tax time, you should receive a 1099-G for your unemployment benefits to report the taxable income on your tax return.

Employer-Provided Life & Disability Insurance – as you may know, Spirit Airlines provided you with a basic one-times-salary group life insurance policy alongside supplemental group life insurance of up to five times your salary. Unfortunately, your life insurance benefits also ended on May 2, 2026, and unless you possess an individual life insurance policy (term or permanent), there is no coverage for your loved ones if something were to befall you.

Solution – your future employer may provide group term insurance similar to the coverage Spirit provided. While there are independent life insurance brokers from whom you could buy coverage (such as Zander Insurance or Policy Genius), you may find it extremely difficult to find affordable coverage given your profession.

As a pilot, you should consider inquiring if an additional policy endorsement / rider is necessary to cover your life in the event of an accident while you fly. Some carriers may limit coverage to non-flying-related incidents.

Additional Consideration – similar to your group life insurance benefits from Spirit, you also received short- and long-term disability insurance through Spirit. Those benefits ceased as of May 2, 2026, as well. Unless you are insured under an individual policy, you are not covered in the event of your disability during your period of unemployment. Seeking an individual policy may also prove beneficial. A financial professional will aid in assessing the policy’s merits based upon your individual circumstances. Once again, disability policies are expensive for pilots.

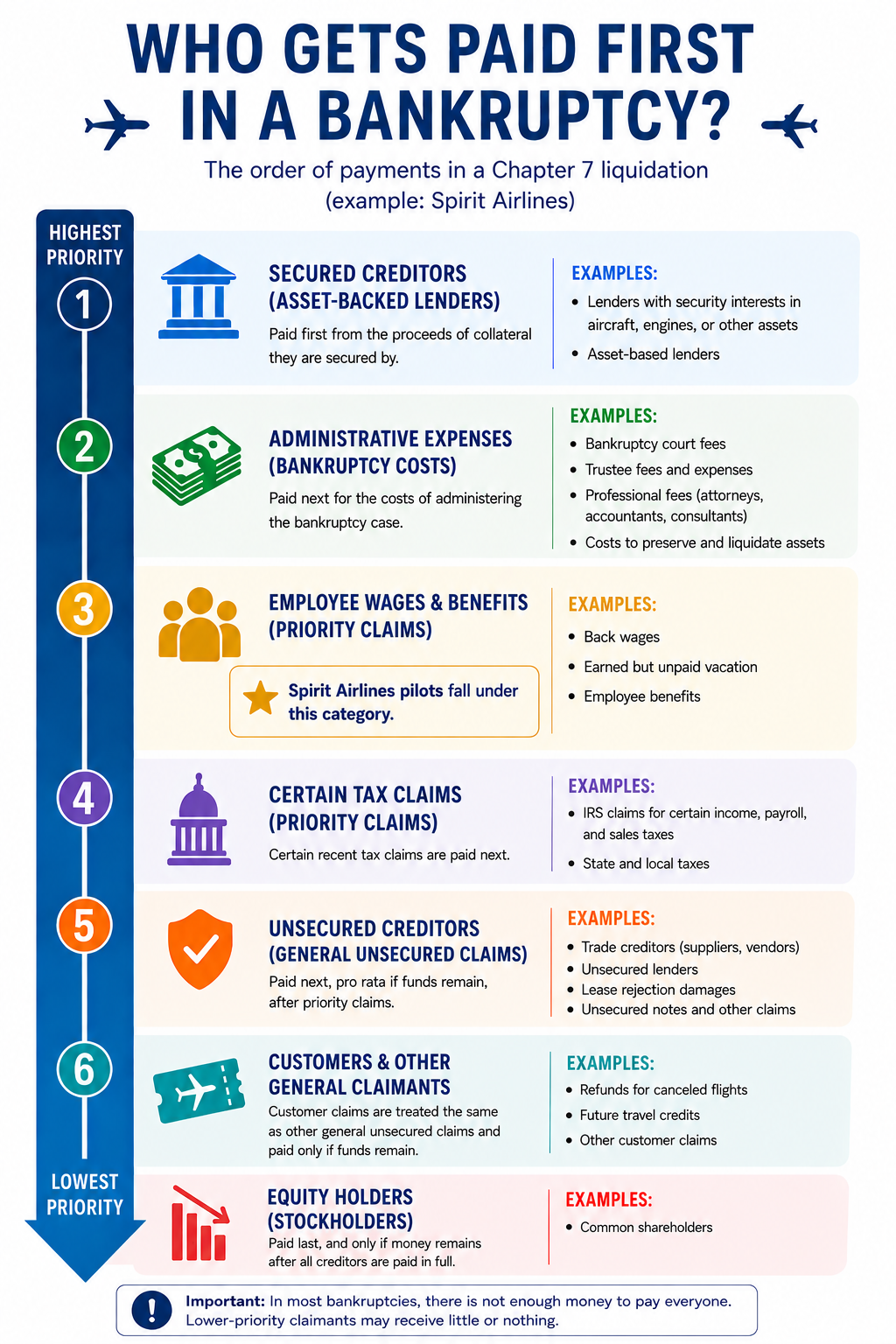

Unpaid Wages / Paid Time Off / Employee Benefits – as you may already be aware, there is a lawsuit filed in Florida seeking restitution for Spirit employees. Even with the lawsuit, it is important to remember the general flow of debt payment when a company files for Bankruptcy.

The aforementioned considerations are not comprehensive, but you are likely to experience greater financial well-being if you attend to each area. A trusted financial planner will walk alongside of you each step of the way as you navigate the time of transition. Additionally, careful planners will help you consider what you may wish to seek in employment with your next flying role:

Considerations Regarding Your Next Flying Role:

Career Path – the airline’s career path is one of the most important factors when selecting a future airline. Evaluate how an airline invests in pilot development, progression, and long-term growth, including upgrade timelines, fleet transitions, and leadership opportunities. A strong structure provides clarity for future income potential, schedule quality, and lifestyle stability, while seniority progression directly shapes daily experience and long-term earnings.

Cash Compensation –like Spirit Airlines, most U.S. commercial airlines follow a similar structure with respect to cash compensation occurring by the hour. Each airline generally guarantees minimum hours (~70-80 hours), and you receive hourly pay during your time from gate departure until gate arrival. If you seek to earn additional compensation, you may pick up additional flying beyond your normal schedule and receive override pay in the process.

Signing and Retention Bonuses – depending on airline need and industry demand, you may benefit from additional compensation to entice you to onboard with a specific airline. Be mindful of the conditions with these “golden handcuffs” in the event you terminate before contractual terms from the airline are met.

Salary – tenured captains are often earning in the $400,000 - $700,000 range at Southwest, United, and Delta, particularly with “overrides,” so there is strong compensation potential if you keep pursuing the profession.

Insurance Options – all the major U.S. airlines (United, Southwest, Delta, and American Airlines) offer medical, dental, vision, life, and disability insurance. As you pursue coverage, consider the following:

Medical – quality coverage carries significant importance, as out-of-pocket healthcare costs can place considerable strain on your finances. Evaluation of an airline’s medical plan requires attention to the type of coverage available, including whether options include a low deductible, high deductible, or both deductible structures. Review the portion of the insurance premium paid by the airline versus your contribution (if any). Moreover, the availability of tax-advantaged accounts such as a Flexible Spending Account (FSA) or Health Savings Account (HSA) adds further value for you.

Dental & Vision – although less critical than core medical coverage, dental and vision insurance still play a meaningful role in a comprehensive benefits package. Employer contributions toward premiums influence overall cost and should factor into your evaluation process as well.

Life – like Spirit Airlines offered for you, most of the major U.S. airlines offer basic and supplementary life insurance for their pilots. The coverage is still considered a group term policy and will often discontinue upon your retirement, the airline ceasing operations, or termination. Even so, you may find difficulty being insurable as a pilot, so the airline policies are often the best choice.

Disability – you will find the majority of U.S. airlines offer short- and long-term disability insurance policies comparable to the offerings at Spirit Airlines. Strongly consider reviewing the specific benefits within the policies and note these benefits would also end upon retirement, the airline ceasing operations, or termination.

Retirement plans – outside of cash compensation, the retirement benefits available with your future aviation employer are likely the most important consideration. Each airline’s retirement plan offerings differ, but most U.S. commercial airlines offer the following plans:

401(k) – like your Spirit 401(k), most other U.S. airlines offer non-elective (you do not need to contribute to receive the benefit from your employer) contributions to a 401(k) between ~15% (e.g., Frontier) ~18% (e.g., Southwest) as part of your compensation package. Spirit contributed 8% of your compensation to your 401(k).

Market Based Cash Balance Plan (MBCBP) – this is a retirement plan which looks like a pension but behaves more like an investment account. The airline contributes a set amount (often a percentage of your pay), and the balance grows over time based on underlying plan investments. The MBCBP is often used to provide additional retirement savings beyond 401(k) limits, and the balance can typically be rolled into an IRA when you leave or retire.

Profit-Sharing Plan – to incentivize employees to partake in the “wins” of the airline, each of the big four U.S. airlines offer a profit-sharing plan. Obviously, profit is not guaranteed each year for a business, but you should take each plan into consideration when choosing your future airline. If you are “maxing out” your 401(k), you may choose to receive the Profit Sharing as cash (e.g., Southwest permits this).

Deferred Compensation Plan (DCP) – each major U.S. airline offers non-qualified (not protected from creditors in bankruptcy) deferred compensation plans. DCPs often allow you to make additional contributions to lower your taxable income if your income is above $360,000.

Other Benefit Considerations:

Stock Options & Employee Stock Purchase Plan (ESPP) – stock option plans often are not available at major U.S. airlines. However, most of the U.S. airlines offer ESPP options for pilots, allowing for up to a 15% discount on company stock purchases. If you desire an in-depth explanation of this offering, our firm recently wrote an article detailing the Southwest Airline’s ESPP offering. Most plans operate similarly to Southwest Airlines’ ESPP.

Time Off Policy – every airline employs different policies regarding time off, relying upon pilots’ monthly schedules, contract-defined minimum days off, sick leave banks, and seniority-based vacation bidding. Review the differing policies across each airline to inform your decision-making process.

Professional Development and Certification Coverage – review the clearly-defined developmental programs offered at the airline and how the airline contributes to your ongoing pilot certification fees (FAA airline transport license, FAA first class medical certification, FCC radio telephone operator, etc.). You may find policy deviations between the different airlines based upon the pilot association’s negotiations with the airline. Mindfulness is important regarding any out-of-pocket costs you must incur to maintain your certifications.

Although losing your position at Spirit Airlines creates uncertainty, the present moment also opens the door to meaningful opportunity for you to achieve a brighter financial future. A disciplined review of compensation, insurance, retirement benefits, career progression, and quality of life places you in a stronger position as you evaluate your next opportunity. Pilots who act with care and who pursue clarity often separate themselves during the hiring process and enter their next role with greater confidence. Careful research today supports stronger financial decisions, steadier long-term progress, and a career path aligned with both professional goals and personal priorities. Our knowledgeable team stands ready to help you understand your current financial status, refine your strategy, and navigate the future with purpose as you seek to achieve your financial goals.

Co-Authors:

Jonathan McAlister, CFP®, CKA®

Justin Reede, CFP®, CKA®

Disclosure: The investment returns of investment securities are subject to various risks and are not guaranteed. Consult with an investment advisor representative for formal investment advice. For tax compliance advice, we recommend you consult with a CPA or Enrolled Agent. For legal advice, we recommend you consult with legal counsel. This blog post should not be considered investment or tax advice. Please note that benefit plans at Spirit are subject to change, and this article may not capture those changes. Integrity Road Wealth Partners LLC is not affiliated with Spirit Airlines Co. in any way.