Southwest Airlines ESPP: What Pilots Need to Know

Amidst the various, valuable workplace and retirement plan benefits available for Southwest Airlines Pilots, an overlooked plan is the Employee Stock Purchase Plan (ESPP). When incorporated properly into planning as a wealth-creation tool, the ESPP functions as a flexible solution, supporting your long‑term retirement savings and allowing you to participate in company share price appreciation at a discounted price. The ESPP is best viewed as a complement to Southwest’s more powerful tax-advantaged plans such as the 401(k), Market-Based Cash Balance Plan, Profit Sharing Plan, and deferred compensation options. For more information regarding the other plans offered through Southwest, you may find our Southwest Airlines Pilot Retirement Plan article edifying.

Properly implemented, the ESPP offers the potential for pilots to buy stock for 10% off the going share price, with the possibility of favorable tax consequences upon sale. Understanding how the Southwest ESPP functions is critical, particularly with respect to contribution limits and tax treatment of stock sales. Professional guidance is often needed to maximize the benefits of the ESPP.

Southwest Employee Stock Purchase Plan (ESPP)

The Southwest ESPP allows pilots who complete six months (or more) of continuous service to purchase Southwest Airlines (LUV) stock through payroll deductions. Payroll deductions are accumulated over an “offering period” designated by Southwest and used to purchase company shares at a discount from the market price (10% discount). Southwest typically invests the contributions toward employer stock monthly (the “offering period”), and the LUV shares are generally held at Fidelity Investments after purchase. It is possible to transfer the shares to a different custodian or to sell them at Fidelity.

ESPP Contribution Limits & Offering Period

When electing a contribution percentage from your salary, you should consider the IRS and Southwest deferral limitations. The IRS limits participation in ESPP offerings to $25,000 per calendar year. Calculations are generally determined based upon the value of the stock at the beginning of each “offering period” (monthly).

Once again, Southwest’s ESPP “offering period” is a fixed window of time during which you contribute to the ESPP via payroll deductions. Over the course of the offering period, your contributions will accumulate with each paycheck. At the end of the period, Southwest will facilitate your purchase of company stock at a discount within the ESPP, using only the contributions accumulated during that specific offering period.

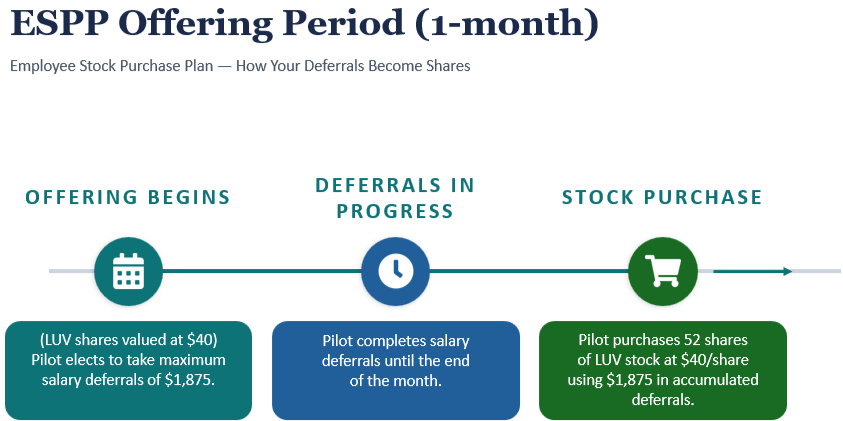

Offering Period Spanning One Month

You may purchase up to (approximately) $2,083 of LUV stock per month, which equals (roughly) 52 shares at $40 per share.

If the ESPP offers a 10% purchase discount, you contribute approximately $1,875 from your monthly paycheck to acquire $2,083 worth of stock. In essence, you receive a “10% off sale” on the company stock.

You are limited to total purchases of $25,000 for the calendar year, inclusive of the 10% discount.

Southwest does not make employer contributions to the ESPP. All purchases are funded exclusively through your payroll deductions. The absence of employer funding further reinforces the ESPP’s role as a supplemental planning tool rather than a primary retirement savings vehicle. Coordinating with a professional team is advantageous when estimating prudent payroll deductions for contribution to the ESPP.

ESPP Taxation

Since ESPP contributions are made on an after-tax basis, no immediate tax deduction is received for contributions. Additionally, Southwest does not withhold federal or state income taxes for ESPP sales activity, meaning you must account properly for ESPP sales activity when filing personal tax returns. The taxation of ESPP stock sales differs from typical brokerage account transactions since certain portions of the sale are taxed at different rates:

Discount Component - the 10% discount is taxed as ordinary income when the shares are sold.

Subsequent Appreciation - any additional gain beyond the discount is taxed either as long‑term capital gain or ordinary income, depending on the holding period.

Taxation Trigger – while you do pay taxes on the amount you contribute toward your ESPP out of your paycheck, you only prospectively pay tax on the share discount and appreciation if the shares are sold.

For more favorable long-term capital gain treatment, the sale must classify as a qualifying disposition:

The stock must be sold more than two years and one day from the offering date.

The stock must be sold at least one year and one day from the purchase date.

If either requirement is not met, the sale will classify as a disqualifying disposition, and the realized gain is taxed at less favorable ordinary income rates (likely 22%-32% for first officers or 32%-37% for captains - at the federal level).

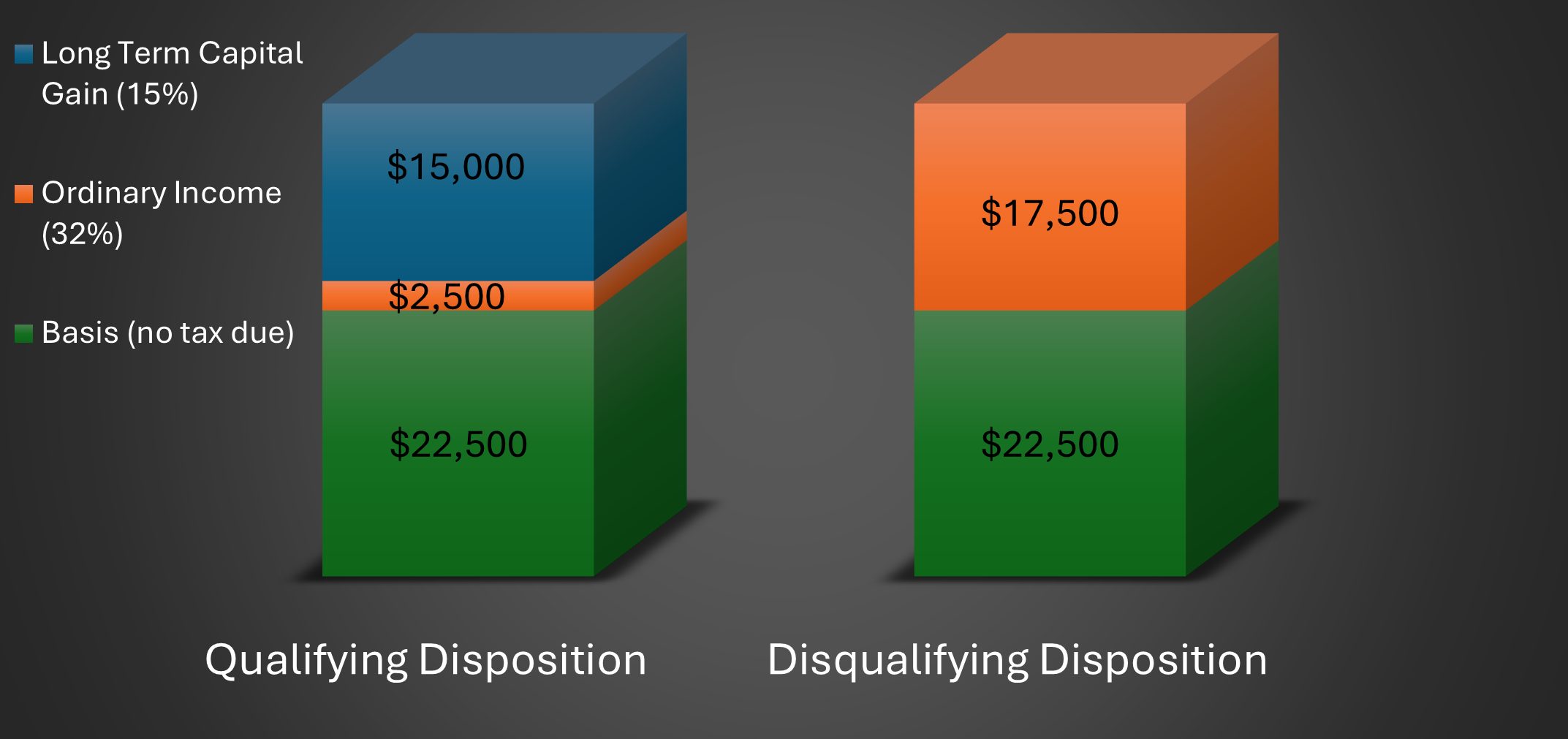

For example, assume $25,000 of LUV stock purchased at a 10% discount through the ESPP is later sold for $40,000. We also assume your ordinary income tax rate is 32%, and your long-term capital gain rate is 15%, which are typical rates given pilot incomes.

If the sale is classified as a qualifying disposition (following the rules noted above), the federal taxation occurs in the following fashion:

Discounted Portion - the pilot paid $22,500 for $25,000 of stock; therefore, the discount of $2,500 is taxed at ordinary tax rates – ($2,500 * 32% = $800)

Realized Gain - the realized appreciation of $15,000 ($40,000 - $25,000) is taxed at long-term capital gain rates – ($15,000 * 15% = $2,250)

The qualifying disposition results in a total federal tax liability of $3,050. If the sale was classified as a disqualifying disposition, the $15,000 in appreciation will be taxed at 32%, resulting in a total federal tax liability of $5,600. Effective timing of ESPP stock sales may reduce your tax liability by 7%-22%, depending upon your tax rate and state of residency.

Proper timing of ESPP sales can significantly reduce taxes as you seek to liquidate timely and to maintain exposure to Southwest at a comfortable level. However, multiple factors, such as projected income, investment strategy within your other investment accounts, liquidity needs for financial goals, and personal financial well-being determine when it is prudent to participate in the ESPP or to sell stock acquired via the ESPP. Our team is glad to assist you in assessing your ESPP participation strategy to support your financial goals.

Coordination with Other Plans & Diversification Considerations

While ESPP participation offers benefits for you, salary deferrals (contributions from income) to your 401(k) and some deferred compensation plans are often more favorable. Through maximum employee deferrals of $24,500 (under age 50) to your 401(k), assuming a 32% marginal tax rate, you reduce your current tax liability by $7,840. You do not receive such a tax deduction when participating in the ESPP, so prioritizing the 401(k) first is wise. An individual stock can fluctuate more than 10% in a matter of days, so you are not necessarily realizing a material benefit from the 10% discount with the ESPP, whereas the tax deduction for the contribution to the 401(k) results in a more straightforward tax savings. Some of the deferred compensation options for tenured first officers and captains also prove superior in certain instances due to their immediate tax savings opportunity relative to the ESPP.

Additionally, participation in your 401(k) provides portfolio diversification (you own dozens or potentially hundreds of different company stocks through your 401(k), while owning Southwest stock increases your exposure to the company’s performance). When evaluating your ESPP strategy, your total portfolio’s exposure to Southwest’s stock performance merits consideration. Southwest is in a stronger market position, but it behooves us to remember Spirit Airlines’ recent bankruptcy in considering how much to concentrate in any one stock. One bankrupt company with 3% exposure in your portfolio hurts, but 20% exposure to a company going bankrupt could materially reduce your flexibility to achieve your financial goals.

Employer performance already influences your income, job security, and retirement benefits, so adding investment exposure to company stock increases the impact of company‑specific swings. A mindful approach often includes setting limits on how much employer stock you hold and steadily diversifying into other investments to maintain balance and reduce unnecessary risk. In the process, you may still benefit from the 10% discount on some share purchases, the amount held in company stock simply requires careful management through periodic liquidations.

The Southwest ESPP is a valuable addition to a comprehensive financial plan when used intentionally and in moderation. Through discounted stock purchases and qualifying dispositions, pilots may realize $7,800 or more (after-tax) per $100,000 of LUV stock in comparison to a typical brokerage investment in Southwest. However, participation in the ESPP requires careful planning and analysis. Due to the complexity of the compensation options and strategies Southwest provides, an expert team is vital to fully evaluate the prudent savings strategy for each individual pilot. An experienced advisor will evaluate whether ESPP participation suits your financial plan, compare the benefits relative to other employer-sponsored plans, provide tax-efficient coordination of sales of LUV shares in the ESPP, and verify proper diversification in the context of your overall portfolio. Ultimately, the ESPP is an excellent tool to help you achieve more goals in the future, but you should consider it in the context of all of your options.

Co-Authors:

Kaden Kozsuch

Justin Reede, CFP®, CKA®

Disclosure: The investment returns of investment securities are subject to various risks and are not guaranteed. Consult with an investment advisor representative for formal investment advice. For tax compliance advice, we recommend you consult with a CPA or Enrolled Agent. For legal advice, we recommend you consult with legal counsel. This blog post should not be considered investment or tax advice. Please note that benefit plans at Southwest are subject to change, and this article may not capture those changes. Integrity Road Wealth Partners, LLC is not affiliated with Southwest Airlines Co. in any way.